1.0Background and Scope

Emerging over tthe last decade in a response to the landfill levy/tax and european demand, exports of refuse derived fuel (RDF) now play a significant role in the management of residual waste in the world.

Over the last 10 years, across the republic of Ireland and the four UK administrations, RDF exports has made beneficial use of residual waste that would otherwise have been disposed to landfill, in lieu of domestic energy from waste (EfW) Capacity.

Despite the rapid expansion in the RDF export market, however, uncertainties exist around the future of the industry. Pressures include the possible implications of rising recycling rates coupled with increased in domestic EfW capacity, as well as the ramifications of Brexit on the economics of export from the UK.

DAERA data shows a relatively stable RDF export tonnage of 140-160 ktpa between 2014 and 2016 for northern ireland, which has the greatest reliance on exports on a per capita basis. In Contrast, Scotland and Wales currently place relatively little reliance on RDF exports.

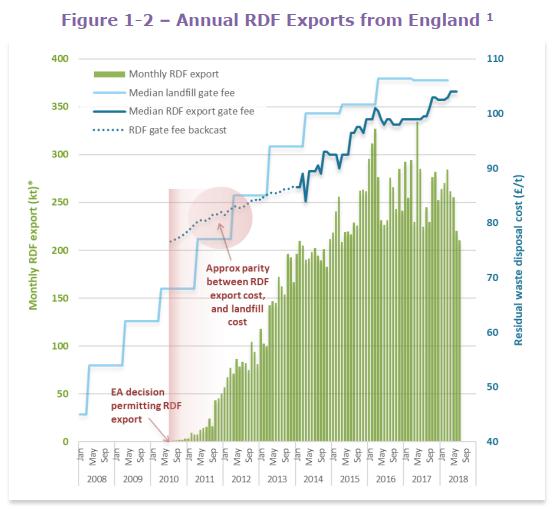

In the case of England, export tonnages appear to have largely plateaued at 3.2 Mtpa over the last two calendar years(see figure 1-2). In fact, the most recent provisional environment Agency datasheet shows a decrease in RDF exports in the year through to July 2018, relative to the year through to July 2017-Though this may be a result of monthly fluctuations, rather than a genuien downturn.

The relativee importance of RDF exports in the waste sectors of each country can be gauged by comparing quantities of RDF exported per capita in each countryOn a per capita basis, Northern ireland currently has the greatest reliance on RDF exports at circa 80kg/person/year, with the republic of ireland ranking second at 70kg/person/year. English exports amount to circa 60kg/person/year, while in scotland and Wales RDF export plays a relatively small role on a per capita basis.

Overarching legislation governing RDF export at EU level is the EC waste shipment regulations (WSR), in tandem with the revised waste framework directive(WFD). Export of RDF for energy recovery is permitted under WSR”amber” waste list, which permits export given prior notice(generally annual) to relevant authorities. Interpretation of the EC waste shipments regulations and enforcement of procedures for RDF export is the responsibility of relevant regulatory agencies in each country.

2.0 What does the market currently look like ?

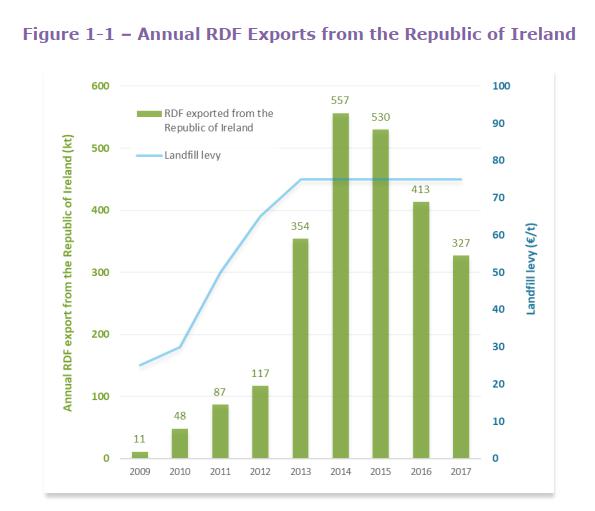

For the case of the republic of ireland, RDF export records show a relatively consolidated market with five companies(Indaver, Greenstar, Greyhound, Panda and Clean Ireland) being responsible for over 90% of the 327 kt exported in 2017. In England, the top five operators (Biffa, Suez,N+P, Geminor and Seneca) account for circa 50% of the 2017 total export of 3.2Mt.

Outflows of RDF from England are predominantly via ports on the East Coast with Dover, Flexstowe and Immingham being the top three ports used by exported volume. While export port data is not available for the republic of Ireland, It is undestood that the significant RDF export routes include the ports of Cork, Limerick, Waterford, Galway and Drogheda.

The Netherlands is currently the largest recipient of RDF from the republic of Ireland(accepting 153kt in 2017), following by Germany (70kt) and Sweden (51kt). The same three countries accept the majority of RDF exported from England, the Netherlands taking the largest volume(1540kt), Germany again ranking second (641kt) and Sweden third (529kt)

Denmark and sweden currently rank as the top export destinations by volume for northern ireland RDF, and notably the republic of ireland ranked as the third major recipient of northern ireland RDF in 2017, receiving 28kt.

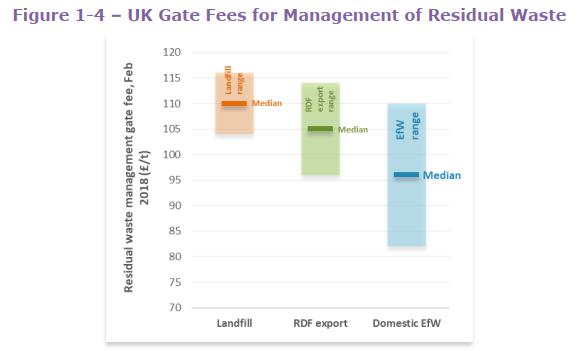

The most recent available data on UK export prices(see figure 1-4) indicates that RDF occupies an intermediate cost niche between landfill (for which tax is the overwhelming component) and domestic EfW, which is relatively inexpensive.

While median prices are clearly stratified, full ranges in the market price for these management options show a significant overlap. For exampel, dependent on geographical location and contract opportunities available, landfill may remain the most cost-effective option in some cases.

2.0What will shape future market demand.

Within the UK, the impact of Brexit remains a significant concern to the RDF export industry. Particular concerns cited include.

--Imposition of tariffs on RDF imports

--Increased friction to RDF movements due to the imposition of customs controls and disruption of process for notifying shipments in the event of a no deal Brexit.

On particular relevance to the issue of tariffs is EC NO.1186/2009, which defines European reliefs for customs duties, and states that “Any consignments made up of goods of negligible value dispatched direct from a third country to a consignee in the community shall be admitted free of import duties”. Given the likelihood that RDF would be classified as having negligible value(effectively having negative value, while the regulation applies a threshold of £150 per consignment). It appears unlikely that a tariff would apply, regardless of the form which Brexit ultimately takes.

At a stakeholder briefing in August, Defra reported that its view, which is supported by HMRC and the world trade organisation(WTO) was that “The export of waste for recovery does not constitute a sale of goods but the provision of a service” and will thereforee not be subject to tariffs.

Nevertheless, the issue of customs controls remains a significant concern.

Following parliament’s rejection of continuing membership of the European union customs Union, the approach to customs controls remains a central matter of contention in brexit negotiations. Future requirements for customs declarations/checks could lead prolonged transit times and additional administrative requirements, increasing the cost of RDF export. The issue of customs controls is clearly particularly critical for movements of RDF/SRF over the Irish border( in 2017, 28kt of RDF/SRF was exported from northern ireland to the republic of ireland)

The long-term future of RDF export sectors in the republic of ireland and uk is also clearly reliant on the ongoing demand for this material in Europe. Sustained demand requires continuing capacity oversupply, which is a function of conditions in recipient countries (largely the netherlands, germany and sweden) including population growth, build out of new EfW capacity, increase in recycling towards EU CEP targets, as well as decommissioning of existing EfW facilies.

Demand for RDF from the republic of Ireland and UK in major recipient countries might also be diminished if export flows from other member states increase in line with the EU CEP, which limits the proportion of residual municipal waste disposed to landfill to 10% by 2030.

3.0 Export Volumes Future Gaze.

To inform understanding of the outlook for exports, Mass balance projections for the waste sectors in the republic of ireland and the uk. In both countries, forecast show that in the event that the EU CEP 2030 requirement for 60% recycling is achieves, RDF exports may contract significantly.

Notwithstanding this overarching finding, differing market conditions prevail in the republic of ireland and the four uk adiministrations. As shown in figure 1-1, it appears that in the republic of ireland new domestic EfW capacity has already begun to impact on export volumes, with further reductions expected in the early 2020s. Assuming that the republic of ireland achieves EU CEP recycling targeted and planned domestic EfW capacity is developed, limited remains residual waste will be available for export in the form of RDF.

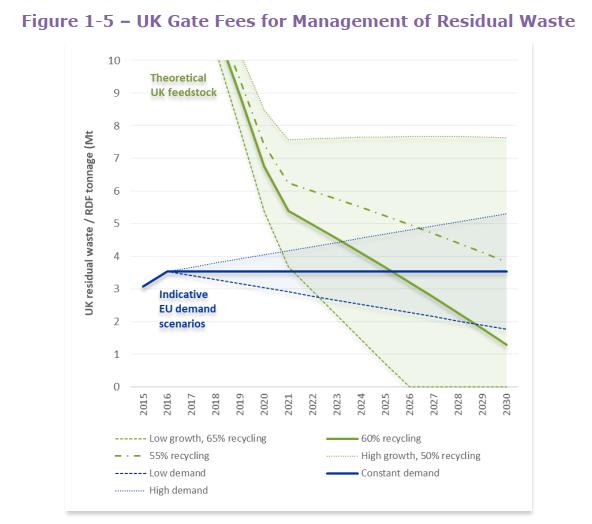

Export volume modelling results for the uk are illustrated in fiture 1-Here, the theoretical uk feedstock(shown in green) is equated to the projected UK capacity Gap, with varying scenearios accounting for possible waste growth and recycling. The requirement for RDF from the EU(shown in blue) is then indicatively projected with scenarios at +/-50% relative to current levels, and a constant case. As shown, supply of residual waste feedstock does not currently directly limit exports from the UK. However, Assuming compliance with the EU CEP target of 60% recycling by 2030(solid green line), constraint to residual waste feedstock supply is likely to put significawtn downward pressure on export levels. These finding are, however, highly contingent on recycling levels ultimately attained by the UK-As shown by width of residual waste forecast envelope (green shaded area)

3.0How should the industry position iteself ?

A range of organisations across public and private sectors are affected by the RDF export market, and will be impacted by future changes in export pricing and volumes. Taking each type of organisation in turn, the impacts is evaluated and strategy considerations is put forward in the context of the evolving RDF market. While this assesement is set out in full in the presidential reports, finding include the following:

RDF exports provide a flexible and potentially economical solution for management of residual waste( for councils not contracted to domestic EfW)

For scottish local authorities, RDF export could present a rapidly deployable solution to meet the requirements of the 2021 ban on biodegradable waste to landfill. It should, however, be noted that some scottish councils may also opt to transport residual waste to landfills or EfW facilities in the North of England.

In northern Ireland, RDF exports potentially provide a relatively low cost disposal option in lieu of domestic EfW capacity. However, having the greatest reliance on RDF exports (when expressed on a per capita basis) northern ireland is also particularly vulnerable to fluctuations in demand, and the potential impacts related to Brexit as outlined above.

In the event of rising RDF export costs( e.g due to devaluation of the pound or onerous customs requirements port-Brexit, regulatory infractions are likely to increase-particularly in relation to time limits on the storage of material as well as the possibility of “orphaned” waste in the event that exporters become insolvent.

In longer term, assuming a decline in overall RDF export volumes, exporters may increasingly look to establish supply agreements with Emerging domestic EfW capacity.

Post time: Jun-03-2020